The Foundation of Your Claim: Identifying Compensatory Damages

At the heart of any personal injury claim is the concept of compensatory damages. These damages are designed to “make the victim whole” again, as much as money can. They aim to reimburse the injured party for all losses incurred as a direct result of the defendant’s negligent or wrongful actions. Understanding the scope of these damages is the first critical step in accurately valuing a personal injury claim.

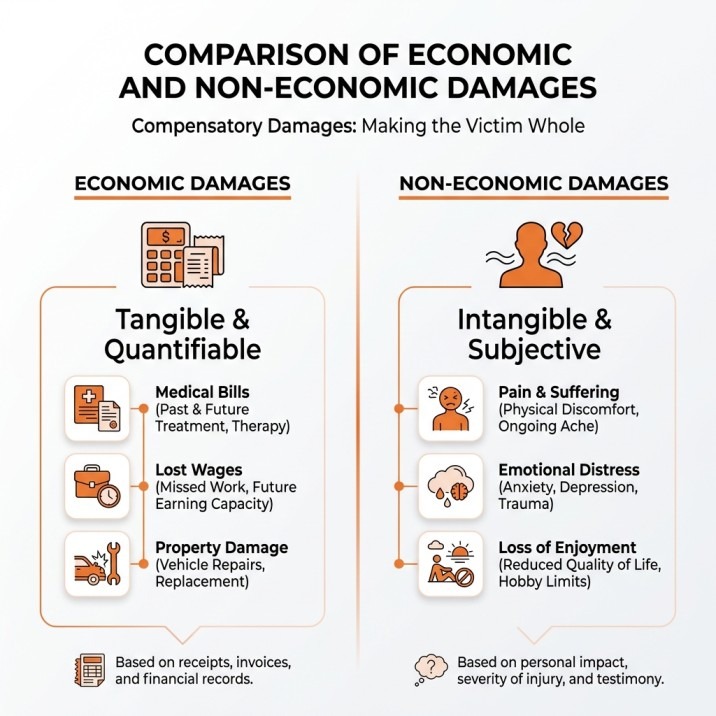

Compensatory damages are broadly categorized into two main types: economic losses, often referred to as “special damages,” and non-economic losses, known as “general damages.” While both are crucial for a fair settlement, they are calculated and proven differently.

Economic losses are tangible and quantifiable. They represent the direct financial impact of your injury. Non-economic losses, on the other hand, are intangible and subjective, covering the emotional and physical suffering that doesn’t come with a bill. Both forms of damage are equally valid and essential to consider when determining the full value of a personal injury claim.

Calculating Special Damages (Economic Losses)

Special damages are the easiest to calculate because they come with receipts, invoices, and clear financial records. These include:

- Medical Bills: This covers everything from emergency room visits, ambulance fees, doctor consultations, prescription medications, physical therapy, rehabilitation, and any necessary surgeries. It’s vital to keep meticulous records of all medical expenses, even those covered by insurance, as you are still entitled to recover these costs. For severe injuries, especially those requiring long-term care, projecting future medical needs is critical. This often involves working with medical experts to create detailed and defensible injury claim projections that account for ongoing treatment, adaptive equipment, and potential future complications.

- Lost Wages: If your injury prevented you from working, you can claim the income you lost during your recovery period. This includes your regular salary, bonuses, commissions, and even missed opportunities for overtime.

- Future Loss of Earning Capacity: This is a more complex calculation, particularly for younger individuals or those with careers cut short by permanent disability. It involves estimating the income you would have earned throughout your career had the injury not occurred, factoring in potential promotions, raises, and benefits. Expert vocational assessments and economic analyses are often necessary for this component.

- Property Damage: In cases like car accidents, the cost to repair or replace your vehicle, as well as any other damaged personal property, falls under special damages.

- Out-of-Pocket Expenses: This category includes any other costs directly related to your injury, such as transportation to medical appointments, assistive devices (crutches, wheelchairs), modifications to your home or vehicle, and even childcare expenses if you were unable to care for your children due to your injury.

The goal here is to compile a comprehensive list of every dollar spent or lost due to the injury. This forms the concrete financial backbone of your personal injury claim.

Quantifying General Damages (Non-Economic Losses)

Quantifying general damages is inherently more challenging because they lack a fixed monetary value. Yet, they often represent a significant portion of a personal injury claim, especially in cases of severe or permanent injury. These damages compensate for:

- Pain and Suffering: This is perhaps the most common non-economic damage. It accounts for the physical pain and discomfort you endured, both immediately after the accident and throughout your recovery.

- Emotional Distress: Injuries can lead to significant psychological impacts, including anxiety, depression, fear, anger, PTSD, and loss of sleep. These emotional tolls are legitimate components of your claim.

- Loss of Enjoyment of Life: If your injury prevents you from participating in hobbies, recreational activities, or daily routines you once enjoyed, this loss can be compensated. This might include an inability to play with children, pursue a career passion, or engage in sports.

- Disfigurement: Permanent scarring, amputation, or other physical disfigurements can have profound psychological and social consequences, for which compensation is sought.

To assign a monetary value to these intangible losses, two common methods are often employed by insurance adjusters and legal professionals:

- The Multiplier Method: This involves multiplying the total special damages by a factor (typically between 1.5 and 5, or even higher for very severe injuries). The multiplier chosen depends on the severity and permanence of the injury, the impact on daily life, and the duration of recovery.

- The Per Diem Method: Less common but sometimes used for shorter-term injuries, this method assigns a daily dollar amount for each day the injured person suffered from the accident until they reached maximum medical improvement.

In Canada, compensation for pain and suffering—formally called “non-pecuniary general damages”—is capped by the Supreme Court of Canada. This cap, adjusted for inflation, is currently just over $430,000 as of 2025. While this specific cap applies to Canadian jurisdictions, it illustrates a legal recognition of the need to quantify such damages, even if the exact figures differ by country and state. In Virginia, while there isn’t a similar hard cap on general damages for most personal injury claims, certain types of cases (like medical malpractice) do have statutory caps.

Factors That Can Increase or Decrease Your Personal Injury Claim Value

Beyond the direct calculation of damages, several critical factors can significantly influence the ultimate value of your personal injury claim. These elements often determine the strength of your case and the willingness of the at-fault party’s insurance company to offer a fair settlement.

The Role of Negligence and Liability in a Richmond Claim

The cornerstone of almost every personal injury claim is proving negligence. Negligence occurs when an individual or entity fails to exercise the reasonable care that a prudent person would have exercised in a similar situation, resulting in harm to another. To establish negligence, we typically need to prove four key elements:

- Duty of Care: The defendant owed a legal duty to the plaintiff to act in a certain way (e.g., drivers have a duty to operate their vehicles safely).

- Breach of Duty: The defendant failed to uphold that duty (e.g., a driver sped or was distracted).

- Causation: The defendant’s breach of duty directly caused the plaintiff’s injuries (e.g., the speeding driver caused the collision that resulted in injuries).

- Damages: The plaintiff suffered actual damages as a result of the injury (e.g., medical bills, lost wages, pain and suffering).

Proving liability is paramount. If liability is clear and undisputed, your claim’s value tends to be higher. However, complications arise with shared fault. Virginia operates under a strict contributory negligence rule. This means that if you are found to have contributed in any way, even 1%, to the accident that caused your injuries, you may be completely barred from recovering damages. This is a significant factor in Virginia personal injury claims and makes proving the defendant’s sole negligence incredibly important.

Identifying all potentially liable parties is also crucial. Sometimes, the direct tortfeasor may not be the only one responsible. For instance, in a commercial trucking accident, liability might extend beyond the truck driver to the trucking company, the cargo loader, or even the truck manufacturer. A thorough investigation can uncover all responsible parties, which is essential for maximizing recovery, especially if one party has limited insurance or assets.

How Accident Type and Severity Impact Valuation

The nature and severity of your injuries, as well as the type of accident, are primary drivers of claim value.

- Minor Injuries: Claims involving minor injuries, such as soft tissue damage (whiplash, sprains) or minor fractures, generally result in lower settlements. In Ontario, for example, minor injury claims often settle anywhere between $10,000 and $50,000. While this is a Canadian statistic, it provides a general benchmark for what constitutes a “minor” claim.

- More Serious Injuries: For injuries like multiple fractures, concussions with prolonged symptoms, or herniated discs, the value significantly increases. These types of claims typically fall between $50,000 and $150,000 in settlements.

- Severe and Catastrophic Injuries: Cases involving permanent disability, traumatic brain injury (TBI), spinal cord injury, significant loss of function, or chronic pain syndromes command the highest values. Settlements for such severe injuries can exceed $250,000 and often climb into the millions, particularly when ongoing medical care, extensive rehabilitation, and substantial loss of income are involved. For instance, the Canadian case of MacNeil (Litigation Guardian of) v. Bryan et al awarded Katherine-Paige MacNeil $18.4 million, with $15 million alone for future care, highlighting the immense cost of catastrophic injuries. Similarly, Gordon v. Greig awarded $23.7 million to two victims for spinal cord and brain injuries.

The type of accident can also influence perception and liability. A pedestrian struck by a vehicle may evoke more sympathy than a single-car accident. A Big rig collision personal injury claim on I-95 or Chippenham Parkway, for instance, often involves more severe injuries due to the sheer size and weight of commercial trucks, leading to higher damages and more complex investigations into corporate liability.

Medical Evidence Strength

The strength and consistency of your medical evidence are paramount. Comprehensive medical records, consistent treatment, and clear diagnoses from qualified medical professionals directly correlate with the perceived legitimacy and severity of your injuries. Gaps in treatment, inconsistent complaints, or a lack of objective findings can significantly weaken your claim.

Insurance Policy Limits

The amount of available insurance coverage held by the at-fault party can act as a practical cap on your settlement. While your damages might be extensive, if the defendant only carries the minimum required insurance and has no significant personal assets, collecting a large judgment can be challenging. This underscores the importance of identifying all potential liable parties and exploring all available insurance policies, including underinsured motorist (UIM) coverage through your own policy.

Venue

The jurisdiction where your case would be tried (known as “venue”) can also subtly impact value. Some jurisdictions are known to be more favorable to plaintiffs than others, potentially influencing jury awards or settlement offers. In Virginia, for example, the specific city or county where a lawsuit is filed can sometimes play a role in the perceived risk and value of a case.

The Importance of Evidence and Documentation

In any personal injury claim, the adage “if it’s not documented, it didn’t happen” rings true. Comprehensive evidence and meticulous documentation are the bedrock upon which a strong, high-value claim is built. Without solid proof, even the most legitimate injuries and losses can be difficult to recover.

Building a Strong Case for Your Richmond Personal Injury Claim

From the moment an accident occurs, every action you take (or don’t take) can impact your claim. Here’s how to build a robust case:

- Gathering Evidence at the Scene: If possible and safe, collect as much information as you can immediately after the accident. This includes contact information for all parties involved and witnesses, insurance details, and photographs or videos of the accident scene, vehicle damage, and visible injuries. For instance, if you were involved in a car accident on Broad Street or a slip and fall in a Richmond establishment, capturing the scene’s conditions is vital.

- Documenting Injuries and Treatment: Seek medical attention immediately, even if your injuries seem minor. A delay in seeking treatment can be used by insurance companies to argue that your injuries were not caused by the accident. Follow all medical advice, attend all appointments, and complete all prescribed therapies. Keep a detailed personal injury journal to record your daily pain levels, limitations, emotional state, and how your injuries affect your daily life. This journal provides a chronological, personal account that can be incredibly compelling.

- Retaining Records: Keep every piece of documentation related to your injury: medical bills, prescription receipts, therapy invoices, lost wage statements from your employer, tax returns (to prove earning capacity), and any correspondence with insurance companies.

- Proving Long-Term Impact: For more severe injuries, demonstrating the long-term impact is crucial. This involves expert testimony from doctors, rehabilitation specialists, and vocational experts who can explain how your injuries will affect your future health, ability to work, and quality of life.

- Demonstrating Financial Losses: Beyond medical bills and lost wages, document any other financial losses, such as property damage estimates, rental car costs, or expenses for household help you needed due to your injuries.

Dealing with Insurance Company Tactics

Insurance companies, while seemingly helpful, are businesses focused on minimizing payouts. They employ various tactics to reduce the value of personal injury claims:

- Quick Settlement Offers: Often, an insurance adjuster will contact you soon after an accident with a lowball settlement offer. They know that you might be financially vulnerable and unaware of the full extent of your injuries or your rights. Accepting this offer prematurely means waiving your right to seek further compensation, even if your condition worsens later.

- Recorded Statements: They may ask you to give a recorded statement. While you are generally required to cooperate with your own insurance company, you are not obligated to give a recorded statement to the at-fault party’s insurer. Anything you say can be used against you to undermine your claim. It’s best to consult with a lawyer before providing any statements.

- Downplaying Injuries: Adjusters may try to suggest your injuries are not as severe as you claim, or that they pre-existed the accident. They might request access to your entire medical history, hoping to find something to discredit your claim.

- Delay Tactics: They might prolong the process, hoping you’ll become frustrated and accept a lower offer.

- Disputing Liability: Even if fault seems clear, they may try to shift some blame onto you, especially in a state like Virginia with its strict contributory negligence rule.

Protecting your rights against these tactics often requires the expertise of a personal injury lawyer. We understand these strategies and can negotiate on your behalf, ensuring you don’t fall victim to unfair practices.

Frequently Asked Questions about Valuing a Personal Injury Claim

Navigating a personal injury claim can be complex, and many common questions arise regarding its potential value and process. Here, we address some of the most frequent inquiries.

What is the average payout for a personal injury claim in Virginia?

It’s a common misconception that there’s a reliable “average” payout for personal injury claims. In reality, there is no set average, either in Virginia or across the country, because every personal injury claim is unique. The value is highly dependent on a multitude of case-specific factors.

As discussed, minor injury claims (e.g., soft tissue damage) will settle for significantly less than severe injury claims (e.g., permanent brain damage or spinal cord injuries). The specific economic losses (medical bills, lost wages) and the impact of non-economic damages (pain, suffering, loss of enjoyment of life) vary wildly from person to person and incident to incident. For example, a young professional suffering a career-ending injury will have a much higher lost earning capacity claim than an individual near retirement with similar physical injuries.

Therefore, instead of focusing on an elusive “average,” it’s more productive to understand the factors that influence your specific claim’s value and to seek a thorough, individualized assessment.

How is pain and suffering calculated in a settlement?

Pain and suffering, as a component of general damages, is notoriously difficult to quantify precisely. While there’s no single formula mandated by law, insurance adjusters and legal professionals commonly use two primary methods as a starting point for negotiation:

- The Multiplier Method: This is the most prevalent approach. It involves multiplying the total amount of your special damages (medical bills, lost wages, etc.) by a “multiplier” that typically ranges from 1.5 to 5 (or sometimes higher for catastrophic injuries). The chosen multiplier reflects the severity, permanence, and impact of your pain and suffering. Factors influencing the multiplier include:

- Injury Severity: A broken bone might warrant a 2x multiplier, while a severe traumatic brain injury could be 5x or more.

- Recovery Time: Longer recovery periods, especially those involving chronic pain or permanent disability, lead to higher multipliers.

- Impact on Daily Life: How much your injuries have disrupted your daily activities, hobbies, work, and personal relationships significantly affects this factor.

- Emotional Distress: The extent of psychological trauma, anxiety, or depression resulting from the injury.

- The Per Diem Method: Less frequently used for long-term injuries, this method assigns a specific dollar amount for each day you experienced pain and suffering, from the date of the injury until you reach maximum medical improvement. This daily rate might be based on your daily earnings or a subjective assessment of your suffering.

The “calculation” of pain and suffering is a negotiation. It’s influenced by the strength of your evidence, the skill of your legal representation, and the willingness of the insurance company to settle fairly.

Should I accept the first settlement offer from an insurance company?

In almost all personal injury cases, the answer is a resounding no. Here’s why:

- Initial Offers are Low: Insurance companies are in the business of making a profit, and their initial offers are almost always designed to be as low as possible. They hope to settle quickly before you fully understand the extent of your injuries, your long-term prognosis, or the true value of your claim.

- Unknown Future Costs: Immediately after an accident, the full scope of your injuries and their long-term consequences may not be apparent. Accepting a quick settlement means you waive your right to seek additional compensation if your medical condition worsens, new complications arise, or you require future surgeries or therapies that were not initially anticipated.

- Lack of Legal Representation: Insurance adjusters are trained negotiators. If you are unrepresented, they know you may not be aware of all your rights or the complex legal processes involved. They will leverage this knowledge to their advantage.

- Importance of Full Valuation: A proper valuation of your claim requires a thorough investigation, collection of all medical records and bills, assessment of lost wages and future earning capacity, and a clear understanding of non-economic damages. This process takes time and expertise.

We strongly advise against accepting any settlement offer without first consulting with an experienced personal injury lawyer. A lawyer can provide an objective evaluation of your case, handle all communications and negotiations with the insurance company, and fight to ensure you receive the full and fair compensation you deserve. The potential consequences of not seeking legal advice can be severe, often leading to significantly undervalued settlements that leave victims with unpaid bills and ongoing suffering.

Conclusion

Accurately valuing a personal injury claim is a multifaceted process that demands a thorough understanding of legal principles, meticulous documentation, and strategic negotiation. It’s about more than just adding up medical bills; it’s about accounting for every way an injury has impacted your life, both financially and personally.

We’ve explored the foundational elements of compensatory damages, distinguishing between the quantifiable economic losses and the more subjective non-economic suffering. We’ve also highlighted the critical factors that can sway a claim’s value, from the clarity of negligence and the severity of injuries to the strength of your medical evidence and the tactics employed by insurance companies. Virginia’s strict contributory negligence rule makes proving liability without any shared fault particularly crucial.

The journey to a fair settlement can be challenging, but with diligent evidence collection, a clear understanding of the valuation process, and the right legal guidance, you can pursue the compensation you rightfully deserve. Our ultimate goal is to ensure that victims of negligence are made whole, allowing them to focus on recovery without the added burden of financial stress. If you’re navigating the complexities of a personal injury claim, especially here in Richmond, understanding these elements is your first step towards securing a just outcome.

Leave a Reply